· Greenback· Spending

The Quiet Crisis in American Wallets

Consumer spending keeps climbing to new records, and so does the credit card debt fueling it. Here's what the latest Federal Reserve data tells us, and why it matters for your money.

The Quiet Crisis in American Wallets

If you feel like everything costs more than it used to, you're not imagining it. But the more telling story isn't really about prices, it's about how Americans are paying for them. Behind the steady drumbeat of "consumer spending hits new high" headlines is a quieter, more uncomfortable trend: a growing share of that spending is being financed with debt that households are increasingly struggling to repay.

The Federal Reserve publishes the data that tells this story in plain numbers. And the numbers are worth a closer look.

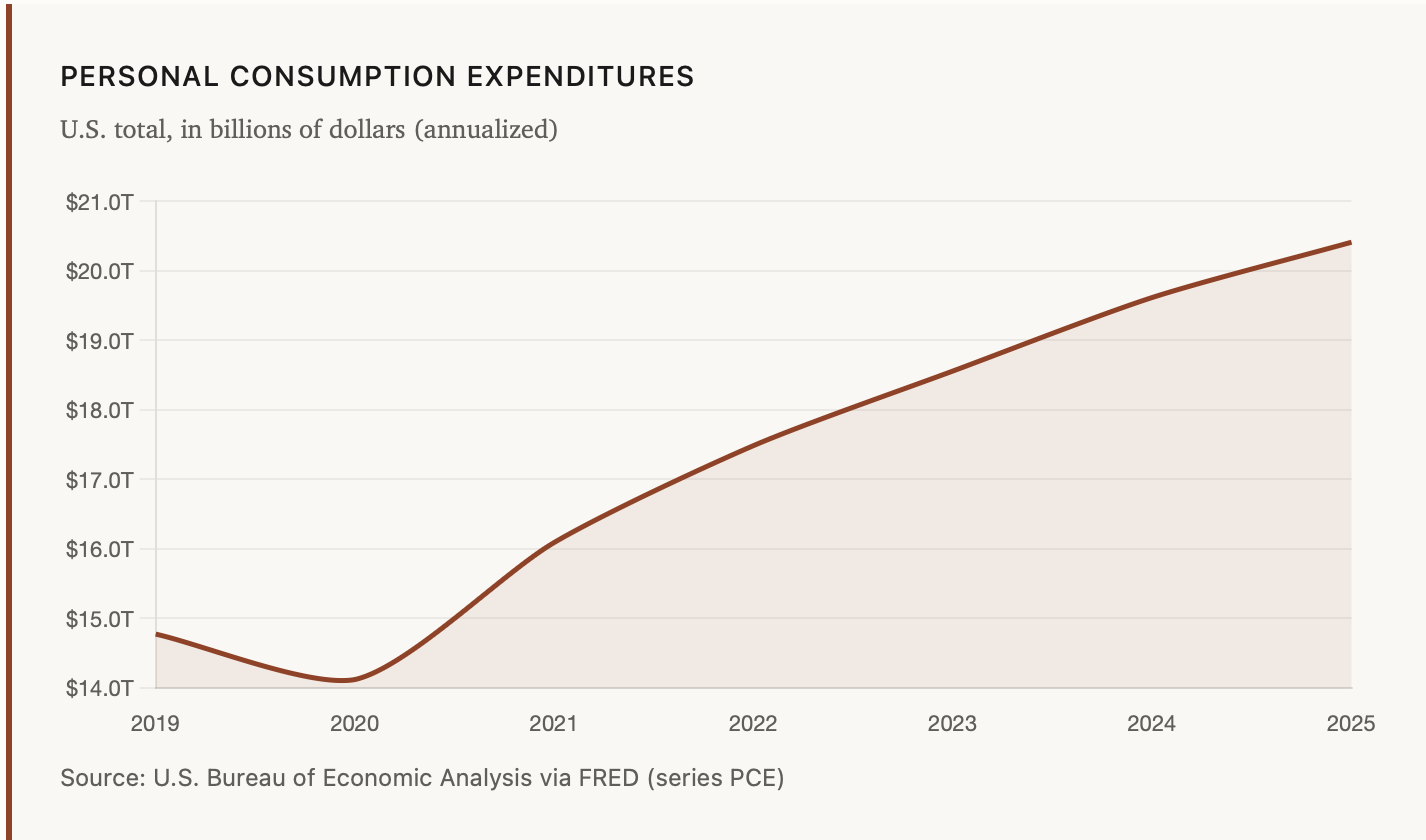

Spending keeps breaking records

Personal Consumption Expenditures, the broadest measure of what Americans spend on goods and services, has set a new all-time high nearly every quarter for the last several years. As of the most recent FRED release, PCE sits above $20 trillion on an annualized basis, up roughly 25% from pre-pandemic levels.

Some of that growth is healthy, population grew, wages rose, the economy expanded. But a meaningful slice of it reflects something less reassuring: prices outpaced paychecks for a long stretch, and households filled the gap with plastic.

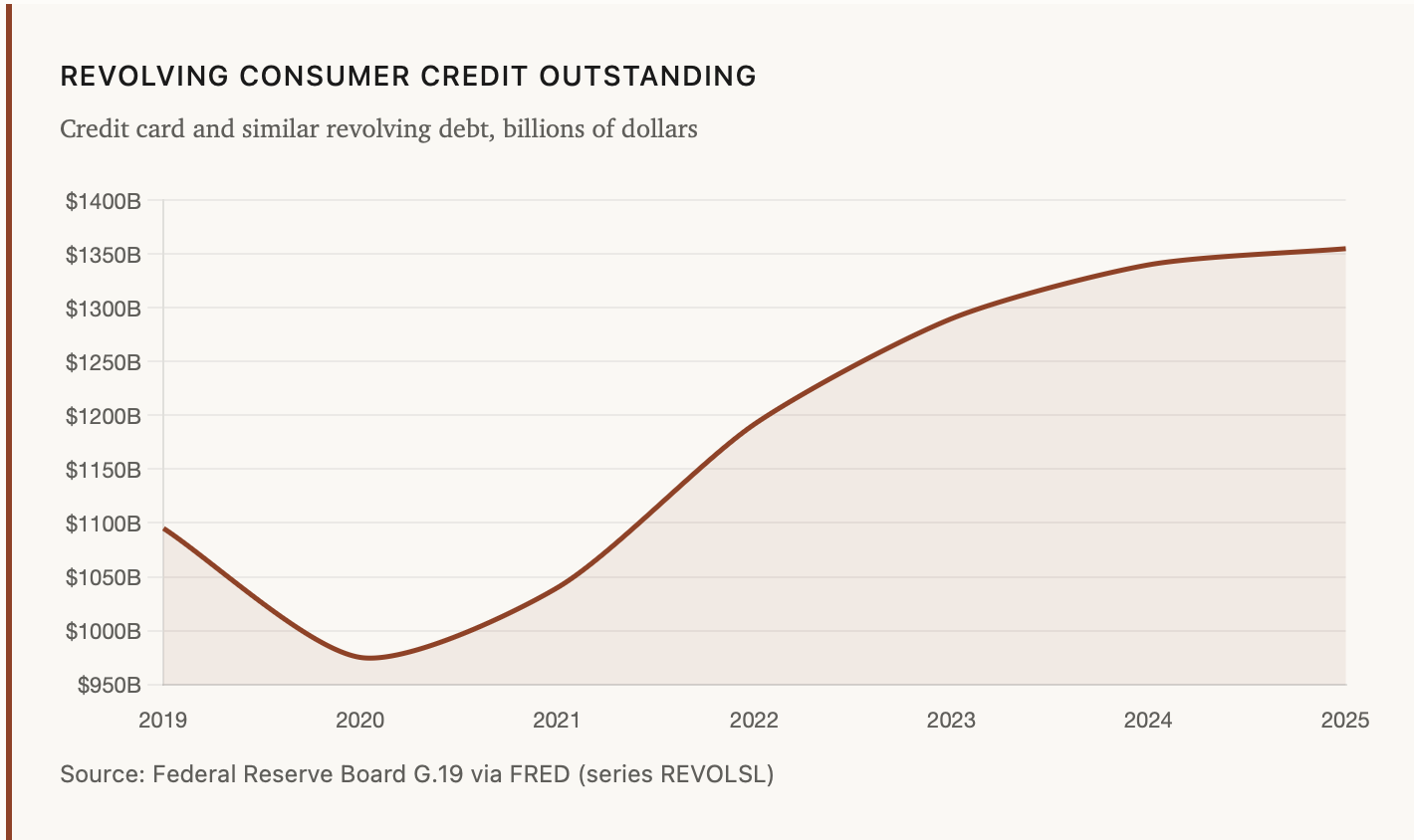

Credit card balances at an all-time high

Total revolving consumer credit, dominated by credit cards has climbed past $1.3 trillion, the highest level on record in both nominal and inflation-adjusted terms. The trajectory since 2021 has been nearly vertical.

Two things make this especially difficult for households. First, the average APR on credit cards is hovering above 21%, which is the highest the Fed has recorded since it started tracking the figure in the 1990s. Second, more of this debt is being carried month-to-month rather than paid in full. Interest is no longer a fee a few people pay; for tens of millions of households, it's a recurring line item.

The average household carrying a balance is paying more in credit card interest each year than they spend on a typical month of groceries.

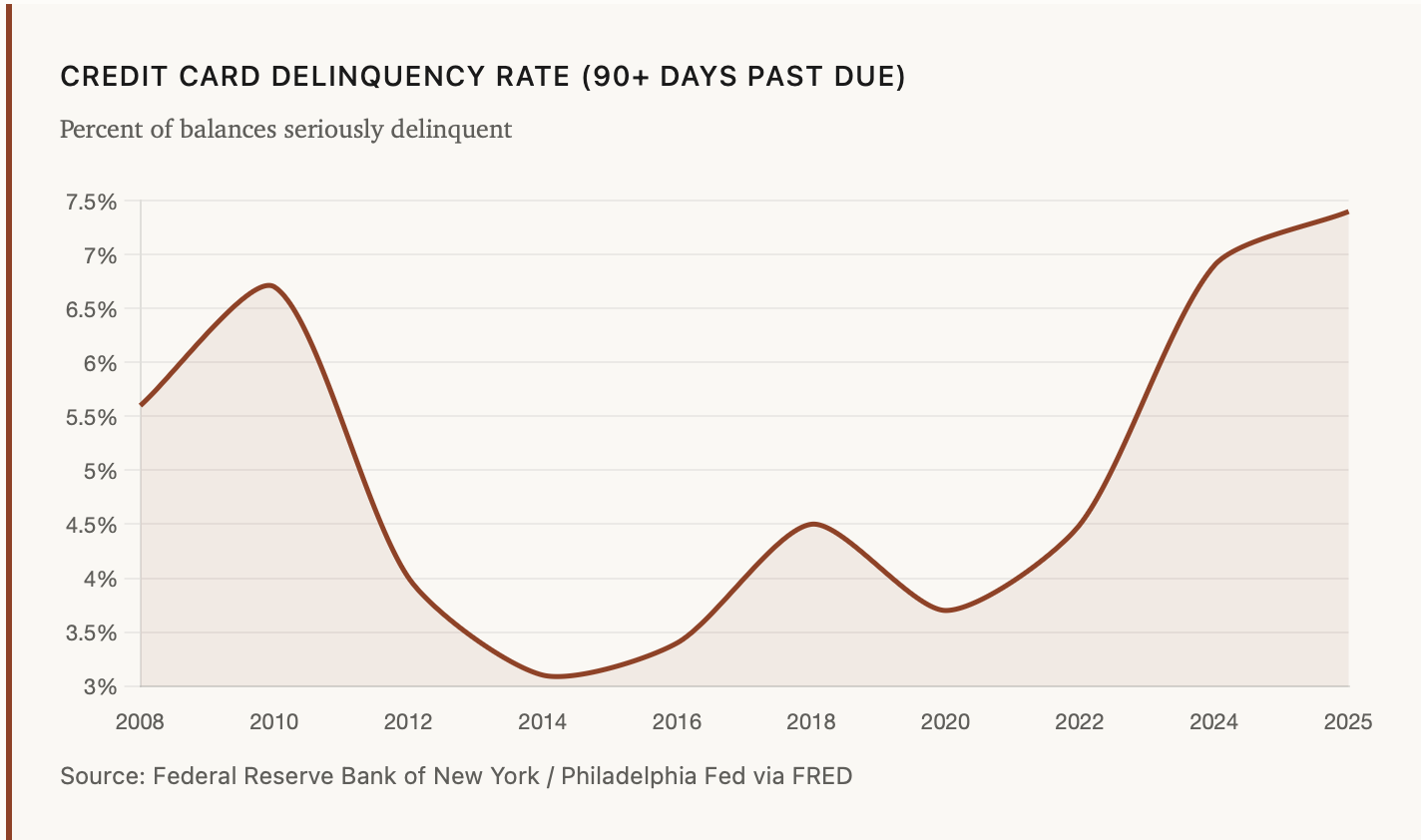

Delinquencies are rising fast

The clearest signal that this debt is becoming unmanageable shows up in delinquency rates. The share of credit card balances 90+ days past due has now climbed above its 2008-2009 financial-crisis peak, a milestone that received remarkably little attention given its historical weight.

Auto loan delinquencies are following a similar path. Serious delinquencies on auto loans (90+ days past due) have climbed to their highest level in roughly three decades, with younger borrowers, those under 40 which are driving most of the increase. Mortgage delinquencies remain comparatively contained, partly because home equity is high and partly because most existing mortgages were locked in at lower rates. But the cracks elsewhere matter, because credit card and auto debt are the early-warning systems for household financial stress.

What this means for the average consumer

It's tempting to read these charts as macroeconomic abstractions. They aren't. They describe the financial reality of tens of millions of households who are spending more, financing more of that spending, and increasingly falling behind on the bills.

The takeaway isn't doom. It's awareness and the recognition that the cultural default has quietly shifted toward financing lifestyle rather than affording it. Reversing that drift starts with the same things personal finance has always recommended, just applied with sharper attention:

Where to start

• Audit the recurring stuff first. Subscriptions, streaming, app fees, "convenience" services, all these compound silently and rarely deliver proportional value.

• Treat credit card interest as the emergency. At 21%+ APR, every dollar paid above the minimum returns more than almost any investment available to retail investors.

• Separate "spending up" from "lifestyle up." Spending more because prices rose is not the same as upgrading your standard of living. Distinguishing the two is the first step to selective reduction.

• Watch the trend, not the month. One high-spend month is normal. A six-month upward trend in credit card balances is a signal worth acting on.

Records get broken. The question is which ones you want to be part of, the spending chart, or the household that quietly stopped financing its way through it.

All data referenced in this post is publicly available through FRED (Federal Reserve Economic Data) at fred.stlouisfed.org. Series referenced: PCE, REVOLSL, DRCCLACBS, DRSFRMACBS. Figures reflect the most recent releases at time of writing; readers can pull current data directly from FRED for the latest values.